Delayed Overshooting — Is the Exchange Rate Puzzle an '80s Artifact?

A sign-restricted SVAR across 14 currency pairs shows that delayed overshooting in response to US monetary shocks is concentrated in the Volcker era (1979–87) and largely absent from post-1987 data.

Background

Rüdiger Dornbusch’s 1976 overshooting model remains the benchmark for understanding exchange rate dynamics after monetary shocks. The core mechanism is uncovered interest parity (UIP): if a central bank tightens unexpectedly, the domestic interest rate rises above the foreign rate, and rational investors require the exchange rate to appreciate above its new long-run level today so that the expected future depreciation satisfies

With sticky goods prices, this means the exchange rate overshoots the new long-run equilibrium on impact, then depreciates smoothly back. The prediction is a sharp, immediate jump followed by monotone decline.

Eichenbaum and Evans (1995) examined post-Bretton-Woods data with a recursive VAR and found the opposite timing: the US dollar appreciation after a contractionary shock peaks 2–3 years later, not on impact. This “delayed overshooting puzzle” attracted two decades of theoretical explanations — non-rational expectations, habit formation, portfolio balance channels, liquidity effects — none of which resolved the timing without auxiliary assumptions.

The puzzle also sits uncomfortably alongside the UIP failure literature: in the full-sample data, the Fama (1984) puzzle shows that high-interest-rate currencies appreciate further rather than depreciate, the reverse of what UIP predicts. Kim, Moon, and Velasco ask whether both anomalies share a single root cause: sample heterogeneity across monetary policy regimes.

Core Idea

The identifying insight is that the Volcker disinflation (1979–87) was unlike the subsequent two decades of US monetary policy in one crucial way: credibility was genuinely uncertain. Markets understood that the disinflationary tightening might be reversed before completion, because the Fed had reversed course during previous episodes. This uncertainty created a forward-looking risk premium — investors demanded persistent dollar appreciation as compensation for the risk of early policy reversal. The resulting exchange rate path looks like “delayed overshooting” but is actually a prolonged depreciation risk premium, unrelated to the UIP mechanism.

Once the Volcker period established Fed credibility (roughly after 1987), the risk premium disappeared and the exchange rate dynamics reverted to near-standard Dornbusch overshooting.

Method

Sign-restricted SVAR

The authors estimate a structural VAR with sign restrictions (building on Uhlig 2005; Canova & De Nicoló 2002) on a system containing the US federal funds rate, industrial production, the price level, and the bilateral exchange rate against 14 trading partners. A contractionary US monetary shock is identified by the restrictions that the short rate rises, output falls, and the price level falls for at least the first several quarters after the shock:

The exchange rate response is left unrestricted — the sign of the impact effect is what the paper wants to learn from the data, not impose. This avoids the recursive (Cholesky) ordering controversy that plagued the Eichenbaum–Evans specification, where the placement of the exchange rate last in the ordering mechanically imposed delayed adjustment.

Subperiods

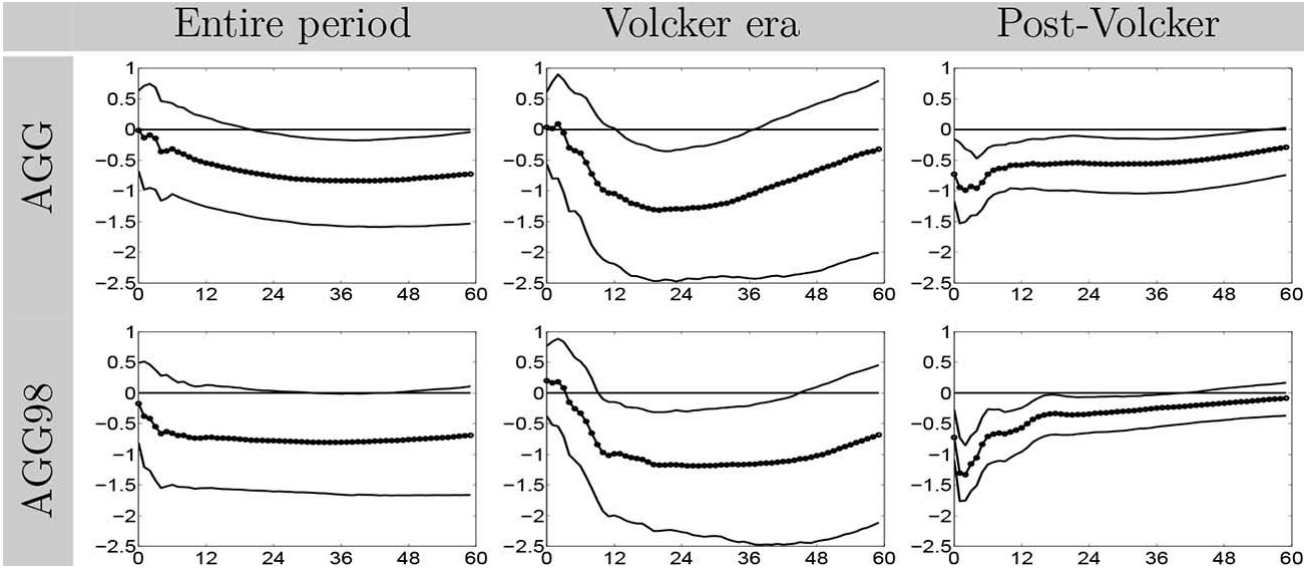

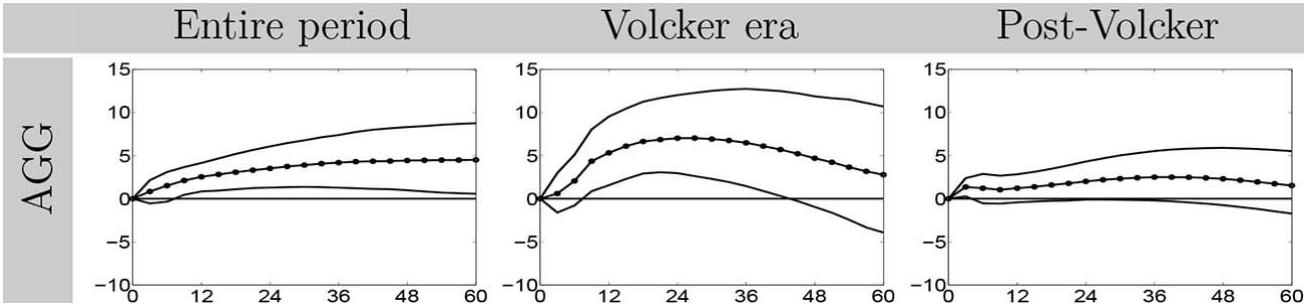

Quarterly data run from 1976:Q1 to 2007:Q4 across the 14 bilateral dollar pairs (G7 plus several OECD economies). Three subperiods are analyzed: the full sample, the Volcker era (1979:Q3–1987:Q4), and the post-Volcker era (1988:Q1–2007:Q4). Impulse response functions (IRFs) are computed for each, along with the conditional UIP test: whether the exchange rate change after the shock is consistent with the interest rate differential at each horizon.

UIP test under the sign-restriction identification

Because the shock is identified without assuming UIP, the paper can test it rather than impose it. The conditional UIP test asks: does equal in the data, conditional on a monetary shock? The answer differs sharply across subperiods, providing an additional discriminating moment over and above the IRF shape.

Experiments

Full sample. The pooled IRF reproduces the Eichenbaum–Evans finding: after a contractionary shock, the dollar appreciates persistently with the peak 6–10 quarters out. The conditional UIP test rejects — the interest differential predicts less appreciation than is observed.

Volcker era. The delayed overshooting is extreme: the dollar appreciates almost monotonically for 2–3 years. The conditional UIP test fails strongly. This is the era of the real dollar appreciation of 1980–1985, which reversed sharply after the Plaza Accord. The low-credibility narrative is consistent: the persistent appreciation reflects a time-varying risk premium demanded by investors who assigned positive probability to policy reversal.

Post-Volcker era. The exchange rate overshoots approximately on impact — the IRF peaks within the first one to two quarters and then declines, consistent with Dornbusch’s prediction. Conditional UIP holds approximately. The “delayed overshooting puzzle” does not appear in this subperiod.

The implication is sharp: pooling the two regimes makes the post-Volcker Dornbusch dynamics invisible because they are numerically dominated by the Volcker-era outlier path. The “puzzle” is a statistical artifact of conflating episodes that belong to distinct monetary policy regimes.

| Subperiod | Peak appreciation lag | Conditional UIP |

|---|---|---|

| Full sample (1976–2007) | 6–10 quarters | Fails |

| Volcker era (1979–87) | 8–12 quarters | Fails strongly |

| Post-Volcker (1988–2007) | 1–2 quarters | Holds approximately |

Limitations

Three caveats worth flagging. First, sign restrictions leave multiple admissible structural shocks on the table; the results hold conditional on the maintained restrictions but alternative sets of signs could, in principle, change the subperiod pattern. The paper uses standard restrictions from the literature, which mitigates but does not eliminate this concern. Second, the credibility narrative is informal: the paper argues the Volcker-era risk premium reflects low credibility, but this claim is not embedded in an identified structural model — it is a post-hoc rationalization of the IRF difference, however economically compelling. Third, post-2007 data — the zero-lower-bound era, quantitative easing, and the return of inflation after 2021 — may constitute a third distinct regime. Whether the post-2007 exchange rate dynamics look like post-Volcker or Volcker-era behavior leaves the puzzle partially open in more recent sample windows.

References

- Original paper: Kim, S.-H., Moon, S., and Velasco, C. (2017). Delayed Overshooting: Is It an ’80s Puzzle? Journal of Political Economy 125(5), 1570–1598.

- Dornbusch overshooting model: Dornbusch, R. (1976). Expectations and exchange rate dynamics. Journal of Political Economy 84(6).

- Foundational puzzle: Eichenbaum, M. and Evans, C. (1995). Some empirical evidence on the effects of shocks to monetary policy on exchange rates. Quarterly Journal of Economics 110(4).

- UIP failure: Fama, E. (1984). Forward and spot exchange rates. Journal of Monetary Economics 14(3).

- Sign restriction methodology: Uhlig, H. (2005). What are the effects of monetary policy on output? Journal of Monetary Economics 52(2); Canova, F. and De Nicoló, G. (2002). Monetary disturbances matter for business fluctuations in the G-7. Journal of Monetary Economics 49(6).

- Response to Kim et al.: Jungherr, J. et al. (2021). Delayed overshooting can still be a puzzle after the 1980s. Economics Letters 199.

- Related work: Kim, S.-H. (2012). Sequential Action and Beliefs Under Partially Observable DSGE Environments. Computational Economics 40(3).